Insurance Snares: Is package plan the best? Should I purchase critical illness insurance or medical insurance for treatment coverage?

Before long, whenever Hong Kong people looked for an insurance plan, they probably contacted their friends who was an insurance agent, claiming they offered the best insurance plans with comprehensive coverage. Yet it was weird that Hong Kong people, who flaunted how smart they were, simply listened and trusted the agents when purchasing insurance plans. They might find that they were “trapped” not until they made any claims because the agents suggested them buying some unnecessary policies for a higher commission. At the end of the day, the one you can trust is only the fact and yourself.

Agents, who are friends of yours or referred by others, suggest insurance plans in package, including life insurance, critical illness insurance, medical insurance, personal accident insurance and hospital cash, and claim that those cover ALL protections. Below is an example:

Majority of Hong Kong people may not identify several serious issues from the above combination. To avoid loopholes, we have summarized three major insurance fallacies which may be encountered:

Fallacy 1: Is “package plan” necessarily the best?

Most agents recommend buying life / critical illness insurance with saving element policies (as known as basic plan), plus a series of Riders (additional contracts), but a good insurance shall never take the form of package.

Under most of the current policies, once the cash value is fully taken out or the insured amount is exhausted, the Riders herein, such as the medical coverage, will be terminated at the same time. Future medical expenses will have to be paid out of your own pocket, touch wood, if you are suffering from any chronic diseases! After the termination of the Riders, a new underwriting procedure is required if you want to buy an insurance policy again while it is possible that extra exclusions or additional loadings will be incurred or even decline will be occurred.

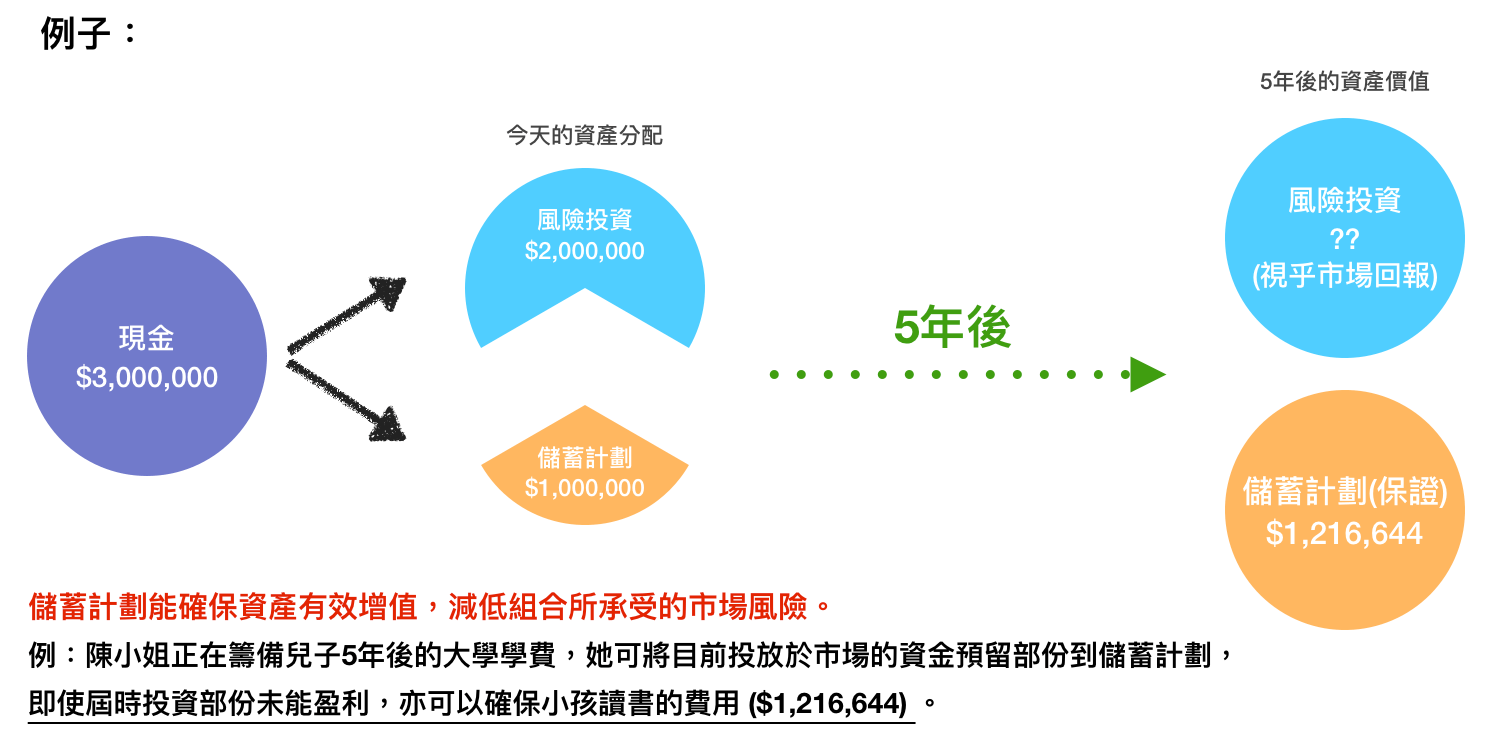

The best way to get a full coverage is to purchase each insurance of different protection’s natures individually. Other coverage will not be affected due to any cash value withdrawn or claims. Plus, you can select the most competitive plan for each nature to maximize the value of the premium you paid. Given an adequate financial situation for investment, you may also replace the policies including saving elements with other forms of investment, and opt for the policies purely for insurance protection. With the significant drop of the premium, you can enjoy a higher level of flexibility on your investment plan.

For example, a 30-year-old non-smoking male has a 25-year unpaid mortgage loan of $1 million, and looks for medical and accidental coverage. Which of the following two plans is more favourable for him?

Package plan from agents

| |||||

Name

|

Insured amount (HKD)

|

Contribution term

|

Protection term

|

Annual premium (HKD)

| |

Life insurance

|

AIA – Executive Life*

|

$1,000,000

|

25

|

Lifetime

|

$12,050

(fixed)

|

Medical insurance

|

AIA – Good Health Medical Plan

|

$124,800^

|

Lifetime

|

Lifetime

|

$2,552

(annual increment)

|

AIA – Supplemental Major Medical

|

$74,800

(80% Reimbursement rate)

| ||||

Personal accident insurance

|

AIA – Accident

Indemnity Rider

|

$240,000

|

35

|

35

|

$1,200

(non-fixed premuimpremium)

|

Total premuimpremium

|

$15,802

| ||||

* Such policy is defined as Basic Plan due to the saving elements therein.

^ The sum of miscellaneous hospital charges, surgeon fee, anesthetic fee, operating theatre fee, fee for cancer treatment & kidney dialysis under medical benefits schedule

| |||||

Optimized combination

| |||||

Name

|

Insured amount (HKD)

|

Contribution term

|

Protection term

|

Annual premium (HKD)

| |

Life insurance

|

Liberty – proLife Series – Term Life Insurance

|

$1,000,000

|

25

|

25

|

$1,410

(fixed)

|

Medical insurance

|

Bupa – CarePro

|

$176,600^

|

Lifetime

|

Lifetime

|

$2,247

(annual increment)

|

Cigna – Plus Medical Plan

(HK$50,000 DedutibleDeductible)

|

$1,000,000

(90% Reimbursement rate)

|

Lifetime

|

100

|

$878

(annual increment)

| |

Personal accident insurance

|

FT Life – "Complementary" Personal Accident Plan

|

$240,000

|

35

|

35

|

$898

(non-fixed premium)

|

Why is there a total discrepancy of HK$10,369 in premium between the two plans?

Under the package plan from agents, you will enjoy $1 million life insurance protection consisting of about $200,000 medical insurance protection and $240,000 personal accident insurance protection. The annual premium costs $15,802. On the other hand, under the optimized combination, a life insurance protection for lifetime will be no longer needed, taking into account the full repayment of the mortgage loan 25 years later. The premium can otherwise be utilized in other areas, for example, you may purchase medical insurance policy which offers you around $1.17 million insurance protection per year, and the final annual premium for such policy costs only $5,433, equivalent to one third of the original. The remaining two-thirds of the premium (i.e. $10,369 a year) can be redeployed freely to generate extra investment return.

Fallacy 2: Is critical illness policy used to cover medical expenses?

Apart from the issues of housing and food, Hong Kong people worry the top three killer diseases: cancer, stroke and heart disease. Therefore, they are willing to pay tens of thousands of dollars yearly for critical illness insurance to ensure medical coverage. Yet the primary function of a critical illness policy is to cover the necessary expenses during the treatment, such as household expenditure, mortgage payment, living expenses and expenses for raising children, instead of paying for the medical treatment!

According to the Hong Kong Cancer Foundation, the market price of targeted therapy at the Hong Kong Hospital Authority and six private hospitals in April 2016 ranges from $0.4 millions to $2.4 millions. The actual cost of treatment will vary subject to the treatment and the length of the treatment. It is assumed that $1 million is needed for breast cancer treatment, so a 30-year-old non-smoking female will be charged $3,125 as annual premium for a medical policy while the annual premium for the critical illness policy is $33,070, equivalent to ten times higher than that of a medical policy!

Thus, if your main concern is the treatment fee, you should opt for a medical insurance to cover your hospitalization and surgery expenses. The real role of a critical illness insurance policy is to cover the expenses instead of the actual treatment cost.

For a 25-year-old young adult who newly join the job market, given that his parents have not retired and he is not married, he bears less economic burdens. If he worries about the issue of unaffordable treatment fee, he should first consider purchasing a medical insurance rather than a critical illness insurance. This also brings to an important point that a package plan may not fit everyone. To effectively transfer the risk to the insurance company, you can look for an insurance policy which is suitable for you. What a waste if you purchase an unfavourable insurance.

Fallacy 3: Is saving element necessarily included in an insurance policy?

Most of us may not aware that a medical insurance and other types of insurance policies can be bought separately and excluded saving elements. But why are there always some saving elements in your policy? And why did the agents not recommend buying a basic plan for protection only? In fact, the agents can sell the basic plan to you but they can earn a higher amount of commission for insurance policies with saving elements. The major function of insurance is to transfer the risks that you can't bear. The more the saving elements in a policy, the less the protection. When the protection is not enough to cover any significant risks, insurance will lose its purpose!

The agents often tend to recommend that you buy insurance with a big chunk of the premium spent on life/savings and critical illness/savings, yet the most important medical insurance protection is overlooked. Even if you suffer from serious illness, you can only pay the treatment by the compensation from critical illness insurance. A policy with saving elements may not necessarily be undesirable, but it is vital that you consider your own needs thoroughly before choosing a suitable insurance product based on your own situation!

In short, at a time information technology boom, devoting time to an in-depth research on financial management and making the necessary comparisons are the best way to make a wise choice, rather than blindly listening to the so-called experts who may end up trapping you with misinformation!

Nothing is more reliable than the fact and yourself.